Comments

VisualMod t1_j9td9tx wrote

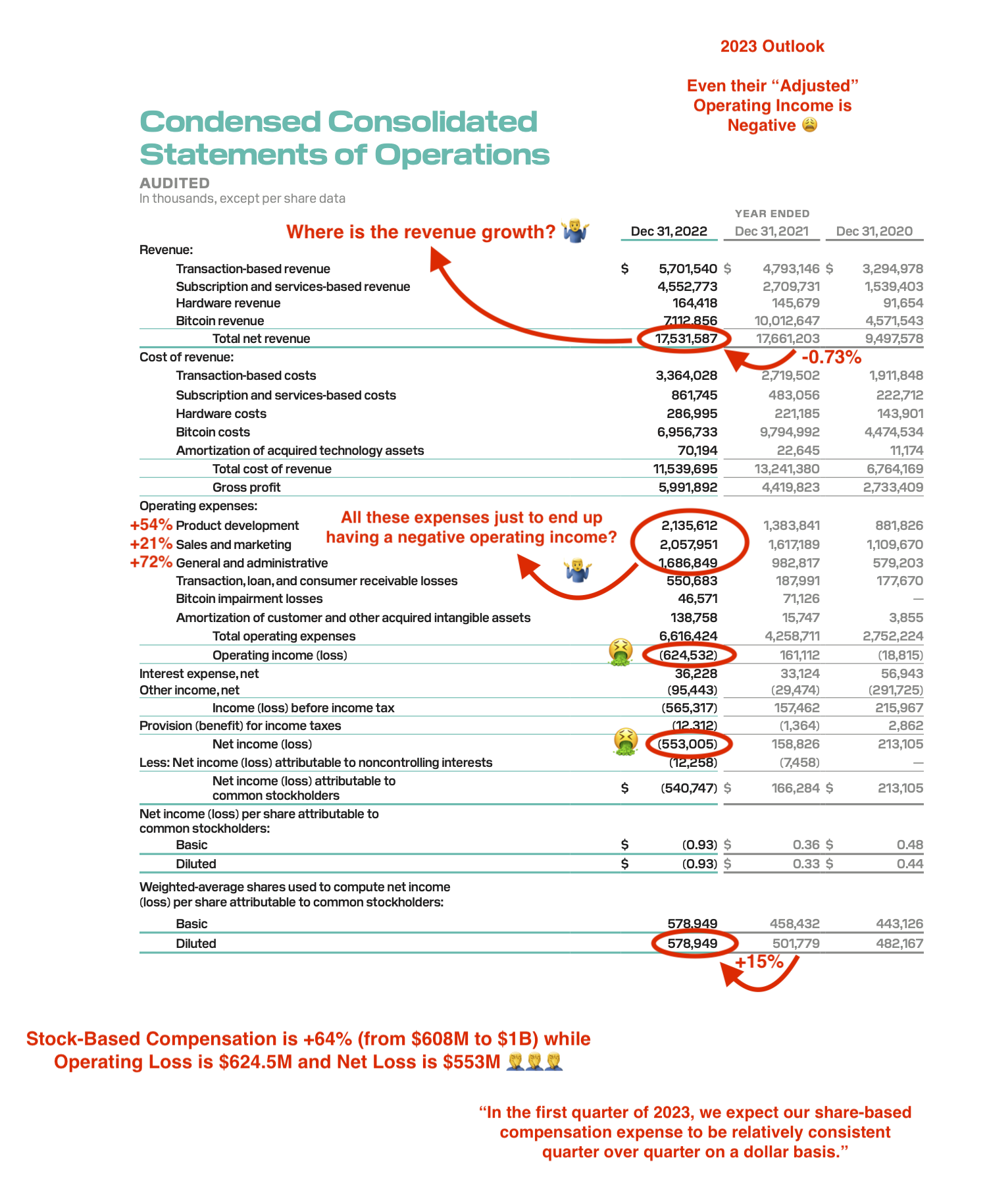

That's a really terrible outlook. They're expecting their share-based compensation expense to increase by 64% while their operating loss is already over half a billion dollars. And their net loss will be even higher. This company is in serious trouble and I wouldn't touch it with a ten foot pole.

Pull-the-trigger t1_j9tdihd wrote

The stock is going up are you hoping you can somehow talk it down to align with your puts?

bovineannilingusfan t1_j9te3jv wrote

I'm embarrassed for you just looking at your posts

FI_investor OP t1_j9tecq9 wrote

Ninja_Gogen t1_j9tedpq wrote

This has Cathie Wood just itching to buy.

GlitteringEar5190 t1_j9thest wrote

Once fed start saying "recession" in meetings, these stocks will plummet. Wait till March meetings and May May be. This market is so similar to 2000s crash.

jer72981m t1_j9thxr8 wrote

All in

computerblue754 t1_j9tk4b1 wrote

If you notice, bitcoin revenue and costs are almost 1:1, which means that that aspect of the business is largely a pass through for cash app customers. I put little value on that initiative. There is really good growth in the core transactions and services businesses. If you don’t believe me, look at how the legacy payment processors are getting crushed by square in the smb space. I would ignore bitcoin in any analysis of the company. Without it revenue was up 30% y/y, which is tough to come by in this economy for tech.

The increase in stock based comp is necessary to keep employees from leaving after last year’s massive decline.

Overall, the valuation is a little rich at 4x core transactions and services sales. But that’s always been the case for square.

[deleted] t1_j9tlmi6 wrote

[removed]

L3G4L_4SS4SSIN t1_j9tr524 wrote

How does that work with extremely low unemployment though? I’m struggling to link the two

laetus t1_j9tvu1v wrote

What did the 2000s crash have to do with unemployment?

Unemployment was low then.

swt5180 t1_j9u0kec wrote

You convinced me, puts it is.

Get ready for it to rocket +25% since I bought puts

Fukitol_shareholder t1_j9u7eos wrote

Numbers. Your numbers show profit. Their numbers, loss. You are done.

Jerund t1_j9u83dc wrote

I think same revenue for 2021 to 2022 is big. In 2021, btc was trading at the peak of 60k a coin. Lots of revenues from that. Now btc in 2022 dropped to as low as 18k at one point and less people trading it. Yet their revenue was consistent. Their core business is growing and factor in after pay acquisition. I see long term potential

FLYWHEEL_PRIME t1_j9ub4sd wrote

Unemployment doesn't mean Jack shit when you can't fill skilled labor jobs because the average IQ goes down year over year.

computerblue754 t1_j9ub6vu wrote

Why is btc a big part of the business when it drives like a 4% margin? Btc revenue was $7.1bn and btc costs were $7.0bn in 2022. The btc business is literally nothing for them.

Jerund t1_j9ubwrw wrote

They invested a lot into btc before the 2020 period and when the value of it increased, they had to report that as income. Think the reporting rules changed under trumps administration. That’s why you have companies like Berkshire report big gains and then big losses. During the btc peak area. They also kinda double down on btc. So when btc drop, they also took a hit.

computerblue754 t1_j9ud2d3 wrote

Are we looking at the same income statement in op’s post? There is no income aside from the transaction fee for handling the trade.

Jerund t1_j9ue032 wrote

What I said earlier was from another source that I read months ago. But speaking back to the income statement posted. You see bitcoin revenue dropped from 10B in 2021 to 7B in 2022. Yes cost for bitcoin also decreased, but for overall growth of revenue, you see it stayed the same for 2021 to 2022. Assuming btc trading didn’t decrease, their revenue for 2022 would be an extra of almost 3 billion dollars.

Andre-ch t1_j9ukwas wrote

check the chart https://tradingeconomics.com/canada/unemployment-rate in 2000s market crash the unemployment rate did not increase.

Andre-ch t1_j9ul32e wrote

i still do not understand why many people focus a lot on the unemployment rate?

Andre-ch t1_j9ul82l wrote

Well said & i confirm

dare2poke t1_j9ule1a wrote

Block’s gross profit is a better proxy for revenue, which is why their investor presentations highlight gross profit instead of revenue.

Payments companies typically trade on net revenue, which nets out transaction costs (mostly interchange revenue they pay to the card networks and issuing banks).

Block’s top-line revenue is gross revenue and transaction costs are included in COGS.

Additionally, for the consumer side, as others mentioned, Bitcoin revenue is largely a pass through because Block buys the Bitcoin that their customers purchase. They make basically no gross profit on their crypto business.

On a net basis, if total revenue is flat, but Bitcoin revenue declined significantly, then it wants their core gross margin positive business is growing.

TLDR - Gross profit is a better proxy for top-line growth, and that grew by 35%

laetus t1_j9ultiy wrote

Because why does it matter?

"Stocks are valued at a billion PE"

-"BUT WHAT ABOUT THE UNEMPLOYMENT"

??

donthaveacao t1_j9upu45 wrote

lol this guy got every bearish play of his wrong and is trying to cope hard

Tasty-Ad-7 t1_j9uqske wrote

another way of saying that employers are unwilling to pay to train in their niche. That the onus is on the prospective employee to already have the skills is the biggest con in America.

Uries_Frostmourne t1_j9wd6a5 wrote

Wonder how afterpay is doing

DeadRater t1_j9wfg30 wrote

agree with this, and if you know your not going to do well on the current year, might as incur your expenses for development and marketing. It will make the next year's statement better if the spending is done in 22 rather than 23.

[deleted] t1_j9xul8b wrote

[removed]

Tasty_Willingness_14 t1_j9yross wrote

That's what you get in an oligarchy. Freedom for me & servitude for thee.

avl0 t1_ja52ep3 wrote

This is like regards first dd or something, what happens when you’re one rung off the bottom of the dunning-kruger curve. 1) flat revenue despite crash in bitcoin is impressive, as is increase in gross margins 2) Dilution was for afterpay acquisition not sbc and don’t use fucking diluted shares you absolute mong.

VisualMod t1_j9td99u wrote